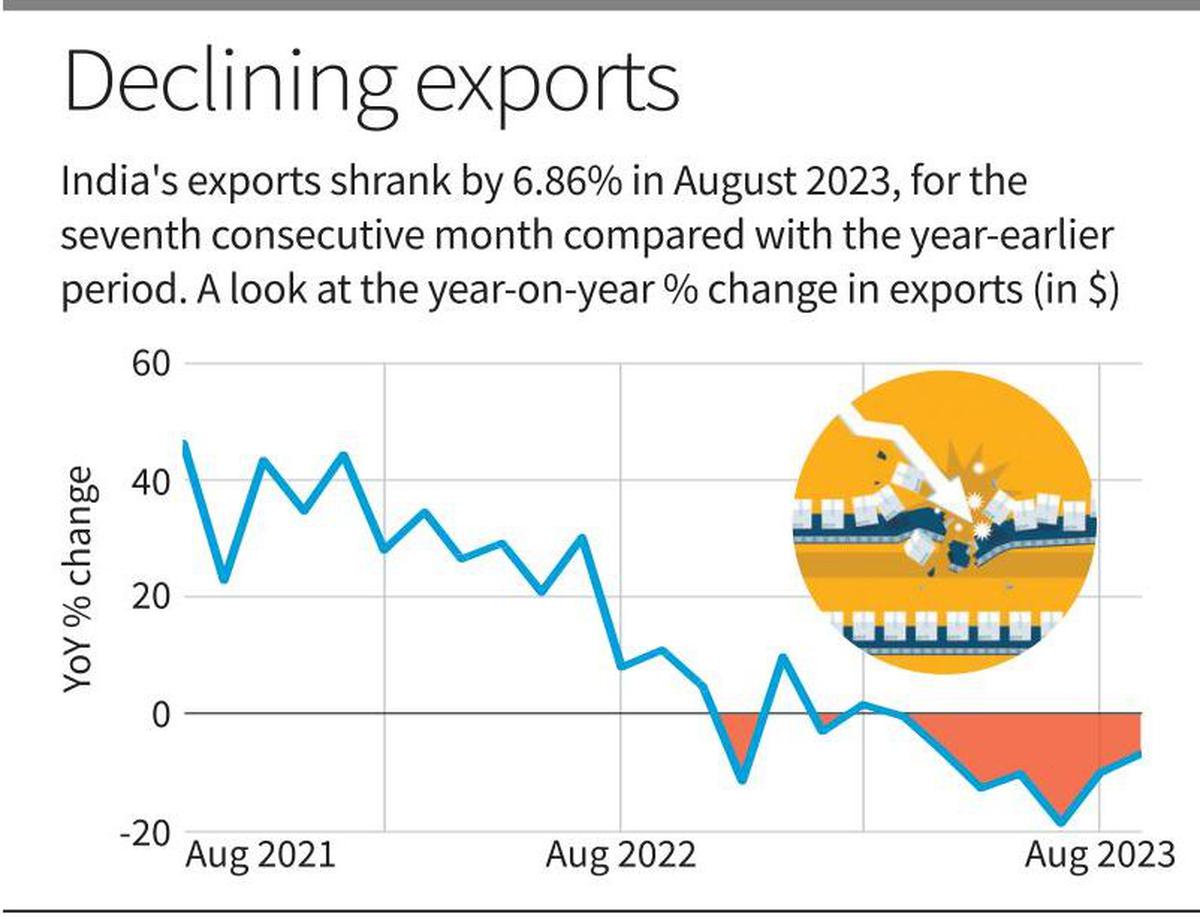

In August, India experienced its seventh consecutive month of decline in merchandise exports, down 6.9% year-on-year, totalling $34.48 billion. According to data released Friday by the Commerce Department, the decline was mainly due to weak external demand. However, the government remains optimistic, saying exports have begun to stabilize, with notable "green shoots".

On the other hand, the goods trade deficit, which represents the difference between exports and imports, hit a 10-month high in August, at $24.16 billion. The increase was driven by rising crude oil prices and strong domestic demand, leading to a nearly 11% month-on-month increase in imports. Imports in August reached 58.64 billion USD, up 5.2% over the same period last year. While exports and imports have been trending downward since the beginning of 2023, the rate of decline has slowed since July.

Commerce Minister Sunil Barthwal pointed out that a high base compared to the previous year also contributed to the decline in exports. Despite the impact of falling commodity prices on export value, export volumes still show a positive trend. Barthwal expressed growing optimism as the industry reported an improvement in export orders and a positive outlook on the export order book. This indicates an overall improvement in the global export scenario. There was also a positive note: non-oil, non-gems and jewellery exports, known as core exports, rose 3.2% in August to $26 billion. However, Barthwal warned that rising oil prices could affect commodity prices and therefore exports in the future.

Aditi Nayar, chief economist at ICRA, predicted that as the goods trade deficit figures for July and August were higher than those for April 2023, the country's current account deficit India in Q2FY24 is expected to exceed the USD 10-12 billion expected in Q1FY24.

In August, merchandise exports fell in 15 out of 30 major sectors. The decline was notable in petroleum products (-30.61%), gems and jewellery (-21.94%), ready-made garments (-8.15%) and organic chemicals and inorganic (-18.83%). However, sectors such as electronics (26.29%) and engineering goods (7.73%) saw growth. Goods imports also fell in 15 out of 30 sectors, including coal (-43.47%), crude oil (-23.76%), and gems (-15.82%). In contrast, gold imports, after a year of decline, increased by 38% to 4.9 billion USD, mainly due to the holiday season.

Federation of Indian Export Organizations President A Sakthivel expressed optimism, saying exports are expected to grow better in the coming months, with new orders and bookings for the Christmas season and New Year. In August, services exports decreased 0.4% to 26.39 billion USD, while services imports increased 9% to 13.86 billion USD, resulting in a surplus of 12.53 billion USD. It is important to note that the services trade data for August is an estimate and will be revised based on the Reserve Bank of India's announcement.

India's trade deficit rose to its highest level since October last year, mainly due to rising oil prices and recovering domestic demand pushing up import bills. The gap between exports and imports reached $24.16 billion in August, surpassing economists' expectations of a $21 billion deficit.

Exports fell 6.9% year-on-year to $34.48 billion in August, while imports were at $58.64 billion, down 5.2%. The decline in exports and imports began to slow in July. Commerce Minister Sunil Barthwal said rising oil prices could impact commodity prices and therefore exports. However, there is still a sense of optimism as exports appear to be stabilizing and the first signs of recovery are becoming apparent.

Following the release of this data, the rupee fell 0.2% versus the US dollar, ending near a record low. Rising inflation in the United States and the European Union, both of which are significant export markets for India, as well as increased interest rates, have impacted demand for Indian goods. Despite the difficulties, the lower rupee versus the dollar and higher oil costs signal strong domestic demand in India, Asia's third-largest economy.

© Copyright 2023. All Rights Reserved Powered by Vygr Media.